How to Cut Loan Origination Cycle Time in Private Credit (Without Cutting Corners)

Why private credit origination is slow, where the days actually disappear, and how non-bank lenders compress time-to-fund without weakening credit discipline.

David Ellett

Co-Founder & CEO

Share now :

In private credit, speed is not a vanity metric. When a family office or non-bank lender can move from indicative term sheet to funded facility in days rather than weeks, it wins deals that slower lenders never see. Borrowers, often facing a settlement date, a refinance cliff or a time-boxed acquisition, reward certainty and pace. Yet most origination teams quietly accept a cycle time they would never tolerate anywhere else in the business.

The frustrating part is that origination rarely slows down because a deal is genuinely hard to assess. It slows down because the process is fragmented. Understanding exactly where the days disappear is the first step to getting them back.

Where the time actually goes

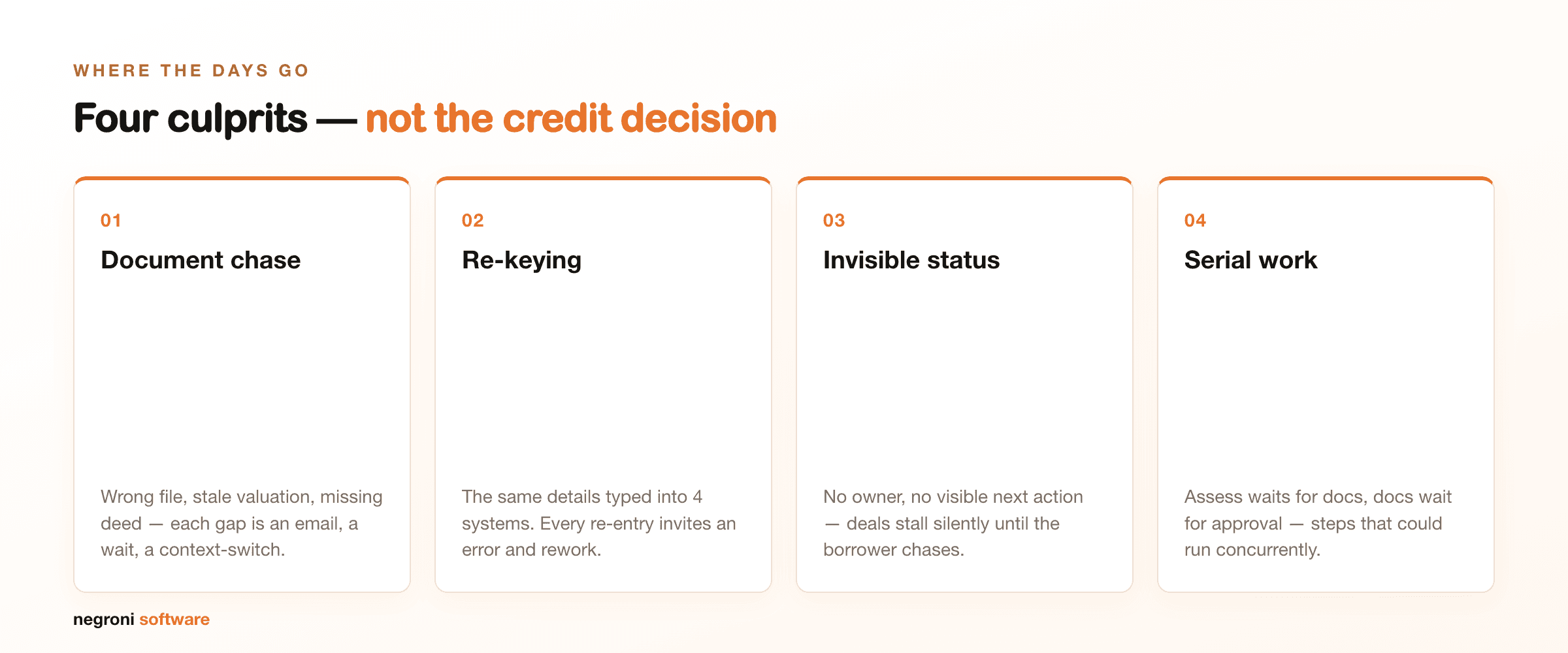

Map a single deal from enquiry to funding and the cycle almost always breaks into the same stages: intake and qualification, information gathering, credit assessment, credit committee or delegated approval, documentation, and settlement. Measure the elapsed time in each and a pattern emerges. The analytical work, the part your credit team is actually paid for, is usually the smallest slice. The bulk of the calendar is consumed by waiting and re-handling. Four culprits dominate.

Document chase. The borrower sends financials, but not the ones you asked for. A trust deed is missing. The valuation is three months stale. Each gap triggers an email, a wait, a follow-up, and a context-switch for whoever picks the file back up. A deal can sit idle for days simply because nobody is actively holding the baton.

Re-keying and reconciliation. The same borrower details are typed into a spreadsheet, then a term sheet, then a facility agreement, then a servicing record. Every re-entry is a chance to introduce an error, and every error found later forces rework upstream.

Invisible status. Ask a fragmented team “where is the Henderson deal up to?” and you often get three different answers. When status lives in someone’s inbox or head, work stalls without anyone noticing, and a deal only re-surfaces when the borrower chases.

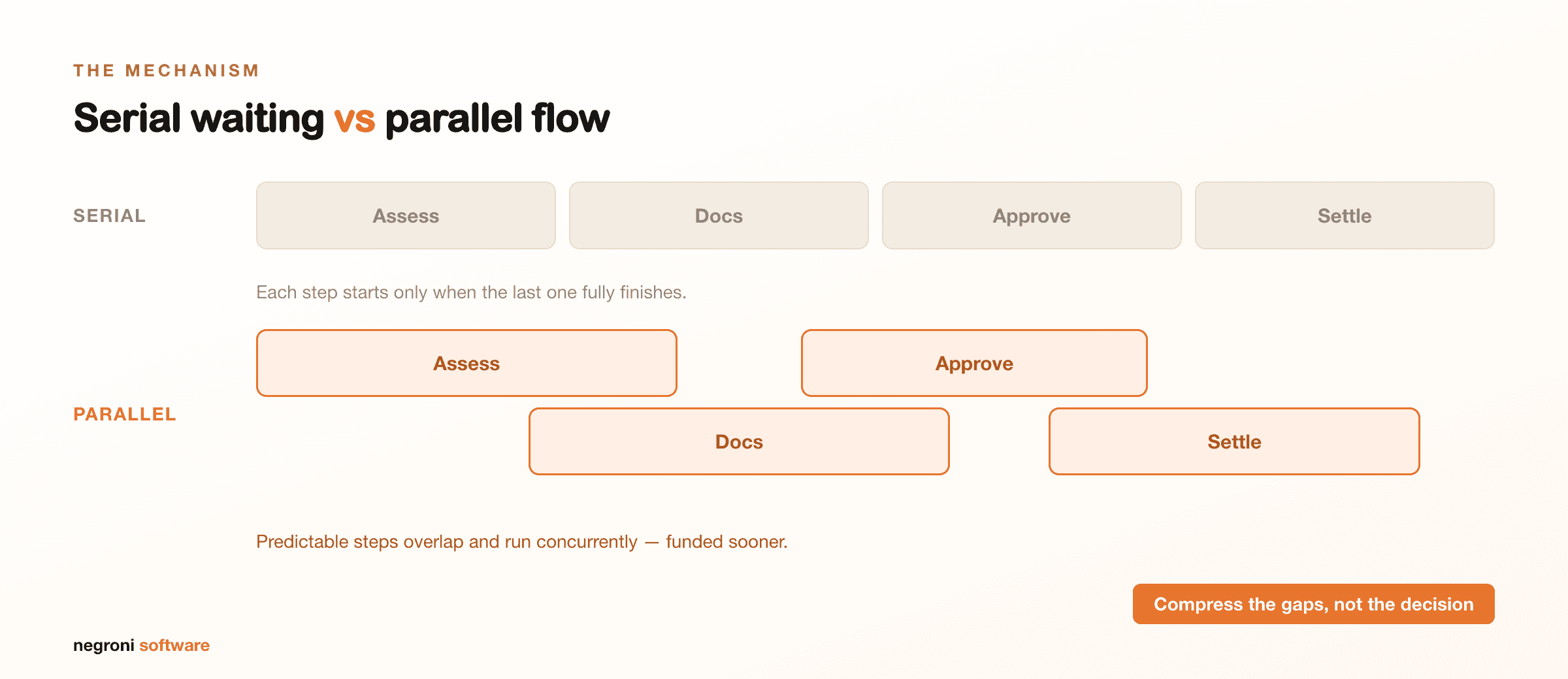

Serial, not parallel, work. Credit assessment waits for documents, documentation waits for approval, and settlement waits for documentation, with each step starting only when the previous one fully finishes. Much of this could run concurrently.

Compressing the cycle without weakening credit

Cutting cycle time is not about approving faster or lowering the bar. It is about removing the dead time around the decision so the decision itself can happen on good information, sooner. Several moves compound.

Standardise intake at the front door. A structured intake, a defined checklist of exactly what a given deal type requires, means the document chase starts complete rather than drip-feeding for a week. If the required trust deed, financials and valuation are specified and requested up front, the borrower can assemble them once. The single highest-leverage change most lenders can make is refusing to let a deal enter assessment until intake is genuinely complete.

Enter data once. When borrower and facility details are captured a single time and flow through to the term sheet, the agreement and the servicing record, you eliminate an entire class of re-keying errors and the rework they cause. This is where a purpose-built loan management platform earns its keep: origination, documentation and servicing draw from one record rather than four disconnected copies.

Make status impossible to lose. Every deal should have a visible position in the pipeline, an owner, and a clear next action. When a file has been idle too long, someone should know without having to ask. Removing “silent stalls” often recovers more days than speeding up any individual task.

Run steps in parallel and automate the routine. Covenant templates, standard conditions precedent and recurring checks do not need a human to start them. Letting the predictable, rules-based parts of documentation and monitoring run automatically frees your team to spend its hours on judgement, the borrower’s real risk profile, rather than administration.

Negroni states that its platform reduces time-to-fund by up to 70% by unifying these stages; whether or not you reach that figure, the mechanism is the same one any lender can pursue: remove the handoffs, the re-keying and the waiting that sit between the real decisions.

Why this matters more in 2026

Two forces make cycle time a board-level issue, not just an operational one. First, competition: private credit has drawn substantial capital, and the differentiator is increasingly execution, not just price. Second, scrutiny: as ASIC sharpens its focus on how non-bank lenders and private credit funds operate, the days of “the process lives in one analyst’s spreadsheet” are ending. A fast origination process built on a single, auditable system is also a defensible one: you can show exactly what was assessed, when, and on what evidence. Speed and rigour, done properly, are the same project.

A practical starting point

You cannot improve what you do not measure. Before buying any tool, do the unglamorous work: take your last ten funded deals and record the elapsed days in each stage. The results are usually uncomfortable and always clarifying. You will almost certainly find that the borrower and the credit team were ready far earlier than the calendar suggests, and that the lost time hid in the seams between systems and people.

That seam is where cycle time is won or lost. Close it, and faster funding follows, not by cutting corners, but by removing the dead space that was never adding anything in the first place.

Frequently asked questions

What is a good loan origination cycle time in private credit? There is no universal benchmark: it depends on deal complexity and facility type. The more useful measure is your own median elapsed days from application to funded, tracked across your last ten deals, and whether the analytical work or the waiting dominates it.

Does cutting cycle time mean lowering credit standards? No. The goal is to remove the dead time around the decision (document chase, re-keying, silent stalls) so the credit assessment happens on good information, sooner. The rigour of the decision itself is unchanged.

Where should a lender start? Measure first. Record the elapsed days per stage on your recent funded deals; most lenders find the largest losses in document chase and serial handoffs, which structured intake and a single system of record address directly.

Ready to see where your origination process is losing days? Book a demo to walk through your own cycle with the Negroni team, or explore Negroni Automation.