Automating Collections and Arrears Management for Non-Bank Lenders

How non-bank lenders and private credit funds automate collections and arrears management: earlier intervention, better cure rates, and NCCP-compliant hardship handling.

David Ellett

Co-Founder & CEO

Share now :

Collections is the part of the loan lifecycle nobody wants to talk about at the fundraising dinner, yet it does more to protect a return than almost anything that happens at origination. A well-priced, well-underwritten book still bleeds if arrears are caught late, worked inconsistently, or handled in a way that trips over Australia’s consumer-credit obligations. For non-bank lenders and private credit funds scaling their books, manual collections is quietly one of the largest sources of both loss and regulatory risk.

The good news is that collections is unusually well suited to automation, not because software can replace judgement in a hardship conversation, but because it can make sure the right conversation happens at the right time, every time, with a complete record behind it.

The real cost of manual arrears management

Picture the typical manual process. A payment fails. Depending on how closely someone is watching the servicing spreadsheet, the miss is noticed today, or next week, or when the monthly review comes around. Someone eventually sends an email or makes a call. Whether a second contact follows, and when, depends on how busy that person is. Notes, if they are kept at all, live in an inbox or a personal file. This creates three compounding problems.

Intervention is late. In collections, time is everything. A borrower who has missed one payment is a very different proposition from one who has missed three, and the probability of curing falls sharply the longer arrears run. Late detection converts a solvable slip into a genuine loss.

Treatment is inconsistent. Two borrowers in identical situations get different handling depending on who happened to pick up the file. That is inefficient, and, where the National Consumer Credit Protection Act applies, it is a compliance exposure, because you cannot demonstrate that hardship was assessed consistently and fairly.

The audit trail is thin. When a regulator, auditor or investor asks how a delinquent position was managed, “it’s in someone’s emails somewhere” is not an answer. The evidence either exists as a system record or it effectively does not exist at all.

What automation actually changes

Automating collections does not mean firing off aggressive demand notices the moment a payment fails. Done well, it means building a consistent, humane, compliant process that runs without depending on anyone remembering to run it.

Detection on day one, not day thirty. The moment a scheduled payment is missed, the position should flag itself and enter a defined arrears workflow. No spreadsheet review, no waiting for the monthly cycle. Early detection is the single biggest lever on cure rates, and it is the one manual processes fail at most reliably.

Staged, rules-based treatment. A missed payment triggers a defined sequence: a reminder, then a follow-up, then escalation to a human, with the timing and channel set by policy rather than by whoever is free. Routine early-stage contact runs automatically; your team’s attention is reserved for the accounts that genuinely need a person. This is the difference between a two-person team managing fifty arrears and the same team managing five hundred.

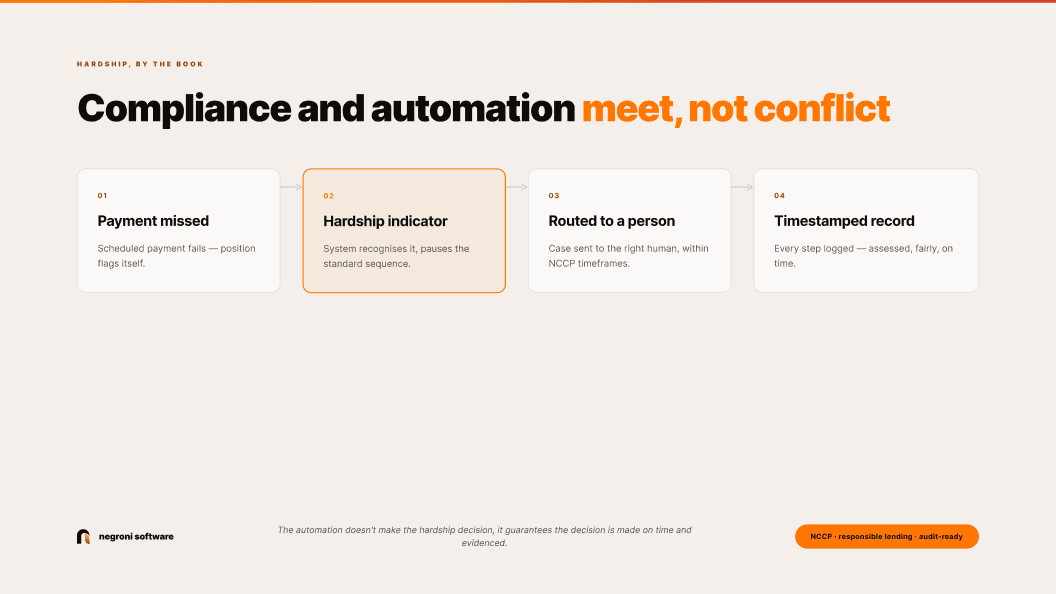

Hardship handled by the book. This is where automation and compliance meet rather than conflict. For regulated lending, the NCCP Act and ASIC’s responsible-lending expectations require that hardship notices are recognised, assessed and responded to within set timeframes, and that the borrower is treated fairly. A system that recognises a hardship indicator, pauses the standard collections sequence, routes the case to the right person, and timestamps every step turns a compliance obligation from a liability into a documented, defensible process. The automation does not make the hardship decision: it guarantees the decision is made on time and evidenced.

A complete, queryable record. Every contact, response, promise-to-pay and outcome sits against the loan. When an investor asks about delinquency in the book, or an auditor tests your collections controls, the answer is a report, not an archaeology project.

The compliance dividend

It is tempting to frame automation purely as an efficiency play: fewer staff, more accounts. That undersells it. As ASIC intensifies its scrutiny of private credit and non-bank lending, the ability to prove that collections and hardship were handled consistently and fairly is becoming as valuable as the efficiency itself. A manual, inbox-based process is not just slow; it is undefensible under examination. An automated, logged one is both faster and safer.

There is a portfolio benefit too. When arrears data is captured cleanly and in real time, it becomes an early-warning system for the whole book. Rising cure times in a particular borrower segment, a cluster of first-payment defaults, concentration building in a stressed sector. All of these are visible weeks earlier when the underlying collections data is structured rather than scattered.

Getting started without boiling the ocean

You do not need to automate everything at once. The highest-return first step is almost always automated early detection and first contact: the day-one flag and the initial reminder sequence. That alone shifts intervention earlier and lifts cure rates, and it frees your team from the low-value chasing that consumes their day. From there, layering in staged escalation, hardship routing and reporting is incremental.

The principle underneath it all is simple. Collections should not depend on someone remembering to look. Build the process into the system, keep the humans for the conversations that need humans, and let the record write itself. Your cure rates, your ops capacity and your next regulatory review will all be the better for it.

Frequently asked questions

Is automating collections compatible with hardship and responsible-lending obligations? Done properly, it strengthens compliance. The system recognises a hardship indicator, pauses the standard sequence, routes the case to a person within NCCP timeframes, and timestamps every step. The automation does not make the hardship decision: it guarantees the decision is made on time and evidenced.

Won’t automated collections feel aggressive to borrowers? No. Automation sets a consistent, humane cadence of reminder, then follow-up, then escalation to a person, set by policy rather than by whoever is free, and reserves your team’s attention for the accounts that genuinely need a human. It is about consistency, not aggression.

What is the highest-return first step? Automated early detection and first contact: the day-one flag and the initial reminder sequence. It shifts intervention earlier, lifts cure rates, and frees your team from the low-value chasing that consumes the day.

Want to see collections run on a schedule instead of on memory? Book a demo with the Negroni team, or explore Negroni Management.