How to Scale a Private Credit Loan Book Without Adding Headcount

How private credit funds and non-bank lenders grow AUM without growing ops headcount linearly: operational leverage, servicing automation and warehouse readiness.

David Ellett

Co-Founder & CEO

Share now :

Every private credit fund and non-bank lender eventually hits the same wall. The strategy is working, capital is available, the pipeline is full, and then someone runs the numbers on what it will cost to service the growth. If managing today’s book takes a team of eight, does tripling the book mean a team of twenty-four? If so, much of the return you fought to originate is about to be eaten by operational overhead.

This is the scaling trap in private credit: for most lenders, operational cost grows almost in lockstep with assets under management. Breaking that link, growing the book far faster than the team, is the difference between a fund that compounds and one that plateaus. It is entirely achievable, but not by working the existing team harder. It requires operational leverage.

Why ops cost scales with the book (when it shouldn’t)

The linear-cost problem is not a law of nature; it is a symptom of how the work is structured. In a spreadsheet-and-email operation, almost every loan consumes a roughly fixed amount of human attention every month: someone reconciles the payment, someone checks the covenants, someone updates the investor report, someone chases the arrears. Double the loans and you double the human-hours. There is no economy of scale because nothing is shared or automated, each position is handled as a bespoke, manual object.

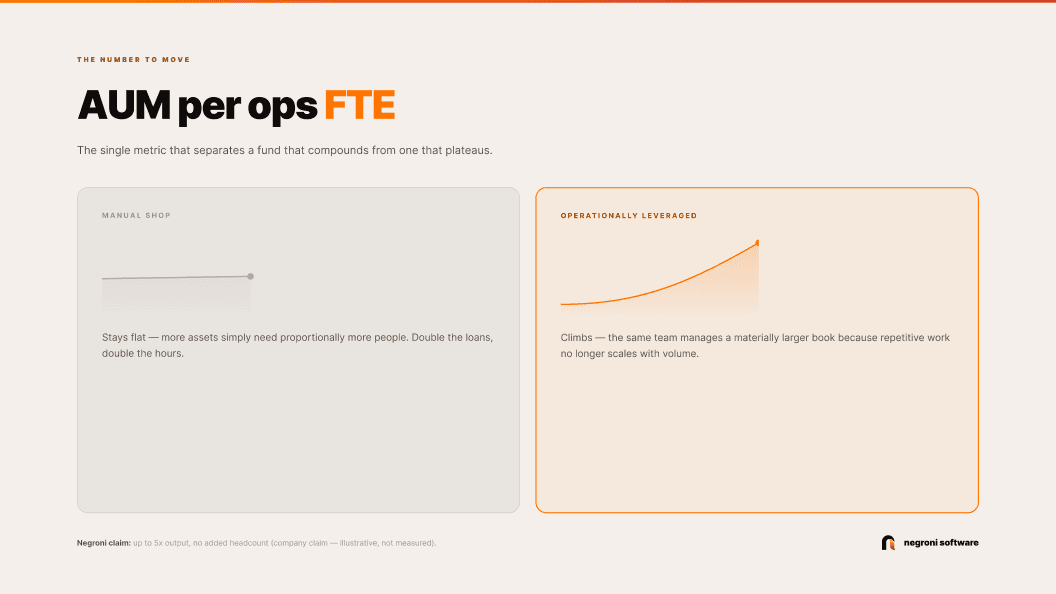

The tell-tale metric is assets under management per operations FTE. In a manual shop it stays roughly flat as the book grows: more assets simply require proportionally more people. In an operationally leveraged shop, that number climbs: the same team manages a materially larger book because the repetitive work no longer scales with volume. Getting AUM-per-FTE to rise is, in one number, the entire objective.

The three sources of operational leverage

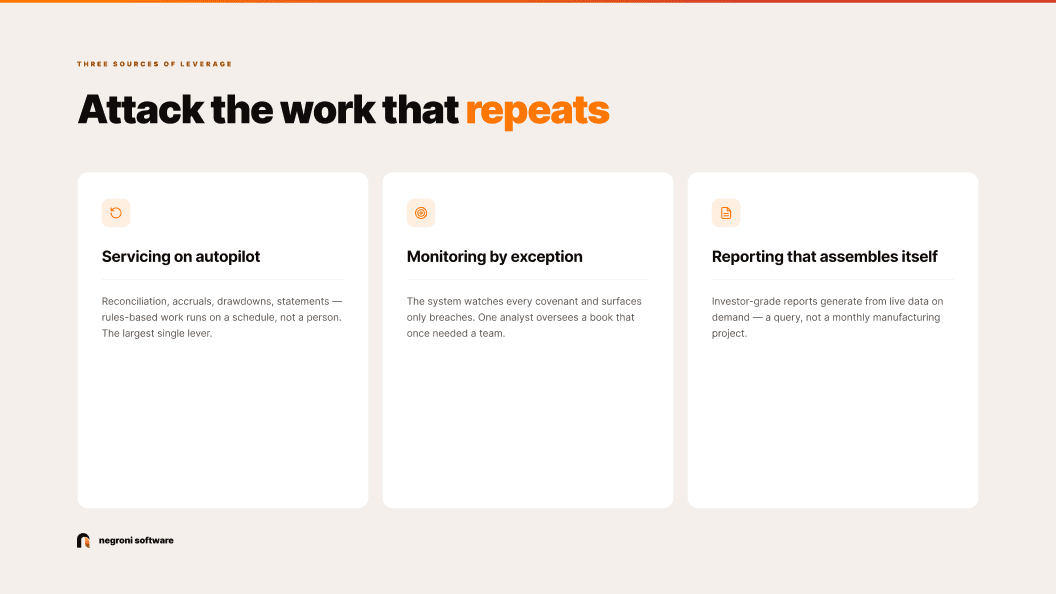

Leverage comes from attacking the work that repeats. Three areas dominate a servicing operation, and each is a candidate.

Servicing on autopilot. Payment reconciliation, interest accruals, drawdowns, fee calculations, statement generation. This work is high-volume, rules-based, and utterly predictable. It is also where manual teams spend an enormous share of their month. When servicing runs on a schedule rather than on a person, the cost of adding the hundred-and-first loan approaches zero. This is the largest single lever, because servicing is the work that most directly scales with book size.

Monitoring by exception. In a manual operation, a person reviews every covenant on every loan because the system cannot. That does not scale. The alternative is monitoring by exception: the platform tracks every covenant and threshold continuously and surfaces only the positions that are approaching or in breach. Your team stops looking for problems and starts responding to them. A single analyst can oversee a book that would have required a whole team to watch line by line.

Reporting that assembles itself. Investor-grade reporting is often the hidden tax on growth. When each report is stitched together by hand from multiple spreadsheets, reporting season means analysts working nights, and every new investor or facility adds to the load. When the underlying data lives in one system, reports generate from live data on demand. The report should be a query against clean data, not a monthly manufacturing project.

Leverage is also what makes you fundable

There is a strategic dimension here that is easy to miss. As a non-bank lender matures, its growth increasingly depends on institutional funding: warehouse facilities, forward-flow arrangements, and eventually securitisation. Every one of those funders and their auditors will interrogate your operational infrastructure before they commit capital. They want to see that servicing is controlled, that covenants are monitored systematically, that reporting is accurate and timely, and that the whole book can be evidenced on demand.

A fund that has built operational leverage has, almost as a by-product, built exactly the infrastructure that warehouse providers and rating agencies require. The same single-system discipline that lets eight people manage a much larger book is what lets a financier get comfortable extending a facility against it. Manual operations, by contrast, are not just expensive to scale; they are a barrier to accessing the very funding that scaling requires. Operational leverage and institutional readiness are the same investment.

The compliance dimension

Scaling manually does not only multiply cost; it multiplies risk surface. Every additional loan handled by hand is another chance for a missed covenant, a late hardship response, or an inconsistent record. As ASIC’s attention on private credit sharpens, a book that has grown faster than its controls is precisely the profile that attracts scrutiny. Leverage built on a single, auditable system means that growth tightens control rather than loosening it: the hundredth loan is monitored exactly as rigorously as the tenth, automatically.

Where to start

The instinct when growth strains the team is to hire. Before you do, look hard at where those hours actually go. For most lenders the honest answer is that the majority of ops time is spent on reconciliation, routine monitoring and report assembly, the three areas most amenable to automation. Automating even the first of them, servicing, typically recovers enough capacity to absorb a meaningful increase in book size with the team you already have.

Negroni claims its customers achieve up to five times the output without adding headcount. The specific multiple will vary by book and starting point, but the mechanism is not magic: it is the removal of the linear relationship between loans and labour. Grow the book, hold the team, and let the system carry the volume. That is how a private credit operation compounds instead of plateauing.

Frequently asked questions

Can a private credit fund really grow AUM without growing ops headcount? Not to infinity, but the near-linear link between loans and labour is breakable. The lever is operational leverage: automating the repetitive servicing, monitoring and reporting work so the same team manages a materially larger book. The metric to watch is AUM per operations FTE: in a manual shop it stays flat; in a leveraged one it climbs.

What should we automate first? Servicing: reconciliation, accruals, drawdowns and statements. It is the highest-volume, most rules-based work and the largest single lever; automating it typically recovers enough capacity to absorb meaningful book growth with the team you already have.

Does operational leverage help with funding? Yes. Warehouse providers, forward-flow funders and rating agencies interrogate operational infrastructure before committing capital. The single-system discipline that lets a small team manage a large book is the same infrastructure that makes the book fundable: operational leverage and institutional readiness are the same investment.

Curious what your team could manage with the repetitive work automated? Book a demo with the Negroni team, or explore Negroni Management and Negroni Analysis.